There are many different types of mortgages available on the market. Some are backed by the government, while others are not. In this blog post, we will discuss government-backed loan programs and what makes them so appealing to borrowers. We will also break down the different types of government-backed loans available and explain how they work. If you are in the market for a new mortgage, be sure to read this post!

Government-backed loan programs are becoming increasingly popular with borrowers. There are many reasons for this, but the most appealing factor is the fact that these loans offer lower interest rates and more favorable terms. Government-backed loans are also more likely to be approved, even if the borrower has less than perfect credit.

There are two main types of government-backed loans: FHA loans and VA loans. FHA loans are insured by the Federal Housing Administration and are available to borrowers with less than perfect credit. VA loans are guaranteed by the Department of Veterans Affairs and are only available to eligible veterans or their surviving spouses.

Both FHA and VA loans have their own set of benefits and drawbacks. Be sure to speak with a loan officer to see if either of these loan types is right for you.

If you are looking for a government-backed loan, contact your local lending institution today! We would be happy to help you navigate the loan process and find the best option for your unique situation. If you need a mortgage lander, I have some terrific ones I work with all the time. Please reach out to me at Middy@ArborMove.com and I’ll be happy to share my short list with you.

Additionally, here’s a short flyer about the different loans, and the benefits of them.

Looking for a place to call home in Ann Arbor? Walden Hills Condominiums may be just what you’re looking for! Our community offers spacious and luxurious one and two-bedroom condos, complete with all the amenities you could dream of. From a swimming pool and fitness center to a playground and picnic area, we have everything you need to feel right at home. Plus, our convenient location just minutes from downtown Ann Arbor makes life easy. Come see us today and find your dream home!

Looking for a spacious and luxurious condo in Ann Arbor? Look no further than Walden Hills Condominiums! Our community offers one and two-bedroom condos complete with all the amenities you could dream of, including a swimming pool, fitness center, playground, and picnic area. Plus, our convenient location just minutes from downtown Ann Arbor makes life easy. Come see us today and find your dream home!

An ideal location near Ann Arbor’s west side and the University of Michigan, Walden Hills is a well-established condo community with ample amenities, as well as a diverse selection of layouts to suit just about any type of buyer. Whether you work in Downtown Ann Arbor, attend college nearby, or are looking to downsize or purchase your first home, you’ll fall in love with the affordable convenience of Walden Hills. Many units have been thoughtfully upgraded throughout the years, and every condo features its own private outdoor space.

Ready to experience everything Walden Hills has to offer? Let’s explore!

Looking for a charming and quiet neighborhood to call home? Look no further than Ives Woods in Ann Arbor, Michigan. This hidden gem is nestled away in the heart of the city and offers a unique suburban feel. If you’re looking for a place to raise a family or retire, you’ll love everything Ives Woods has to offer!

This lovely neighborhood is made up of mostly single-family homes, with a few duplexes and townhouses sprinkled in. The architecture is primarily Mid-Century Modern, which gives the area a unique and stylish feel. The streets are lined with mature trees, adding to the charm of Ives Woods.

One of the best things about living in Ives Woods is its convenient location. You’re just a short drive or walk away from all the shopping and dining that Ann Arbor has to offer. And if you’re looking for some outdoor recreation, you’ll find plenty of parks and nature trails nearby.

If you’re searching for a peaceful and picturesque neighborhood, be sure to check out Ives Woods! This hidden gem is sure to make you fall in love with Ann Arbor all over again.

Any major life change can be scary, and buying a home is no different. Let’s connect so you have an advisor by your side to take fear out of the equation.

Are you in the market for a new house? If so, you know that it can be a daunting task. There are so many things to consider! How do you know if you’re getting the best deal? In this blog post, we will discuss six ways to get the best deal on a house. Whether you’re buying or selling, these tips will help you save money and time!

1. Get pre-approved for a mortgage.

2. Work with a real estate agent who knows the market.

3. Get a home inspection.

4. Research comparable homes in the area.

5. Negotiate!

6. Be prepared to walk away from the deal if necessary.

By following these tips, you will be well on your way to getting the best deal on a house! Happy house hunting!

So, you’re in the market for a new house? Congratulations! This is an exciting time in your life. However, it can also be a bit daunting, especially if you don’t know where to start. Don’t worry – we’re here to help! In this blog post, we will discuss 10 essential tips for buying a house. By following these tips, you will make the process of buying a home much easier and less stressful. Let’s get started!

1. Get pre-approved for a mortgage loan

One of the most important things you can do before beginning your house hunt is to get pre-approved for a mortgage loan. This will give you a clear idea of how much money you have to work with and will help you narrow down your search to houses that are within your budget.

2. Have a realistic budget in mind

When you’re looking at houses, it’s easy to get caught up in the excitement and start considering homes that are outside of your budget. However, it’s important to keep your finances in mind and only look at houses that you can realistically afford. Otherwise, you may end up regretting your purchase later on.

3. Work with a real estate agent, find a good Realtor

If you’re not familiar with the process of buying a house, working with a real estate agent can be extremely helpful. A good agent will be able to guide you through the entire process and help you find the perfect home for your needs and budget. Make sure they are a licensed Realtor. estatereal

4. Know what you’re looking for

It’s important to have a clear idea of the type of house you’re looking for before you start your search. Otherwise, you may end up wasting time looking at homes that don’t meet your needs. Do you want a single-family home? A condo? A townhouse? Make a list of your must-haves and start your search from there.

5. Consider your long-term needs

When you’re buying a house, it’s important to think about your long-term needs. Are you planning on starting a family? Do you envision yourself living in this house for many years to come? It’s important to consider these things before making a purchase so that you don’t end up outgrowing your home too soon.

6. Location, location, location

The old real estate adage still rings true – location is everything! When you’re looking at houses, pay attention to the surrounding area. Is it in a good school district? Is it close to public transportation? Is it in a safe neighborhood? These are all important factors to consider when choosing a home.

7. Don’t forget about maintenance and repairs

When you buy a house, you’re also responsible for maintaining and repairing it. Be sure to factor these costs into your budget so that you’re not caught off guard later on.

8. Pay attention to your gut

When you find a house that you’re interested in, pay attention to your gut feeling. If something feels off, it’s probably best to move on to another property. Trust your instincts – they’ll usually lead you in the right direction.

9. Have a home inspection

Before you finalize your purchase, be sure to have a professional home inspector take a look at the property. They will be able to identify any potential problems that you may not have noticed and can help you make an informed decision about whether or not to buy the house.

10. Don’t rush into anything

Buying a house is a big decision and it’s important to take your time. Don’t feel pressured to make an offer on the first house you see. If you find a property that you’re interested in, take your time and be sure that it’s the right fit for you before making an offer.

By following these tips, you will be well on your way to finding the perfect home for you and your family. Just remember to take your time, do your research, and trust your instincts – you’ll be sure to find the perfect house in no time!

Let’s explore the definition of real estate. What is real estate? This is a question that many people ask, and there is no one answer to it. Simply put, real estate is the physical property that makes up our world. It includes land, buildings, and anything else that has a physical existence. But real estate is more than just a collection of bricks and mortar. It is an investment, a way to generate income, and an essential part of our economy. In this blog post, we will explore the definition of real estate and discuss its importance!

Real estate is defined as the land, buildings, and any other improvements on it, as well as the natural resources that are found on or beneath it. This definition encompasses a wide variety of properties, from single-family homes to commercial office buildings. Real estate can be either residential or commercial in nature. Residential real estate includes properties such as single-family homes, townhouses, and condominiums. Commercial real estate, on the other hand, encompasses office buildings, retail space, warehouses, and industrial facilities.

The importance of real estate cannot be understated. It is an essential part of our economy and plays a vital role in creating jobs and providing housing for families. In addition, real estate generates significant tax revenue for local, state, and federal governments. And, finally, real estate is a key driver of economic growth.

There are many different types of real estate, but they all share one common goal: to provide a safe and comfortable place for people to live, work, and play. We hope this blog post has helped you better understand the definition of real estate and its importance. Thanks for reading!

If you’re thinking about selling your house but wondering if buyers are still out there, know that there are still people who are searching for a home to buy today. And your house may be exactly what they’re looking for.

While the millennial generation has been dubbed the renter generation, that namesake may not be appropriate anymore. Millennials, the largest generation, are actually a significant driving force for buyer demand in the housing market today. Here’s why.

Millennial Homebuying Power

While there’s no denying higher mortgage rates are making it more challenging to afford a home today, many millennials are still eager and able to buy homes – whether it’s their first or they’re moving up. That’s in large part because of the value they place on education.

A recent article from First American says millennials may be the most educated generation in our nation’s history. Because of that, they tend to earn higher wages, and that translates to greater homebuying power. Odeta Kushi, Deputy Chief Economist at First American,explains:

“In 2020, millennials with a bachelor’s degree had a median household income of over $100,000, while those with at least a graduate degree had a median household income of over $120,000. Compare those income levels with the median household income of millennials with just a high school degree (or some college) of $60,000 and the earning power benefits of higher education are undeniable. . . . Millennials’ pursuit of higher education is good news for the housing market. . . because education is the key to unlock both greater earning power and, in turn, homeownership.”

And since wages are one of the key things that factor into affordability when it comes to buying a home, these higher earnings can help millennials achieve their homeownership goals.

Millennials Continue To Be a Driving Force of Demand

A number of studies have looked into how the millennial generation views homeownership and how they’re uniquely positioned to define the housing market moving forward. As the largest generation, the volume of potential millennial homebuyers will have an impact on the market for years to come. As an article in Forbesexplains:

“At about 80 million strong, millennials currently make up the largest share of homebuyers (43%) in the U.S., according to a recent National Association of Realtors (NAR) report. Simply due to their numbers and eagerness to become homeowners, this cohort is quite literally shaping the next frontier of the homebuying process. Once known as the ‘rent generation,’ millennials have proven to be savvy buyers who are quite nimble in their quest to own real estate. In fact, I don’t think it’s a stretch to say they are the key to the overall health and stability of the current housing industry.”

If you’re thinking of selling your house but are hesitant because you’re worried that buyer demand has disappeared in the face of higher mortgage rates, know that isn’t the case for everyone. While demand has eased this year, millennials are still looking for homes. As Mark Fleming, Chief Economist at First American, says in an article:

“While not the frenzy of 2021, the largest living generation, the Millennials, will continue to age into their prime home-buying years, creating a demographic tailwind for the housing market.”

Bottom Line

Millennials are interested in and well-positioned to achieve their homeownership dreams. If you’re ready to sell your house, know that it may be just what they’re looking for.

With all the headlines and talk in the media about the shift in the housing market, you might be thinking this is a housing bubble. It’s only natural for those thoughts to creep in that make you think it could be a repeat of what took place in 2008. But the good news is, there’s concrete data to show why this is nothing like the last time.

There’s Still a Shortage of Homes on the Market Today, Not a Surplus

For historical context, there were too many homes for sale during the housing crisis (many of which were short sales and foreclosures), and that caused prices to fall dramatically. Supply has increased since the start of this year, but there’s still a shortage of inventory available overall, primarily due to almost 15 years of underbuilding homes.

The graph below uses data from the National Association of Realtors (NAR) to show how the months’ supply of homes available now compares to the crash. Today, unsold inventory sits at just a 3.2-months’ supply at the current sales pace, which is significantly lower than the last time. There just isn’t enough inventory on the market for home prices to come crashing down like they did last time, even though some overheated markets may experience slight declines.

Mortgage Standards Were Much More Relaxed Back Then

During the lead-up to the housing crisis, it was much easier to get a home loan than it is today. Running up to 2006, banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance their current home.

Back then, lending institutions took on much greater risk in both the person and the mortgage products offered. That led to mass defaults, foreclosures, and falling prices. Today, things are different, and purchasers face much higher standards from mortgage companies.

The graph below uses Mortgage Credit Availability Index (MCAI) data from the Mortgage Bankers Association (MBA) to help tell this story. In that index, the higher the number, the easier it is to get a mortgage. The lower the number, the harder it is. In the latest report, the index fell by 5.4%, indicating standards are tightening.

This graph also shows just how different things are today compared to the spike in credit availability leading up to the crash. Tighter lending standards over the past 14 years have helped prevent a scenario that would lead to a wave of foreclosures like the last time.

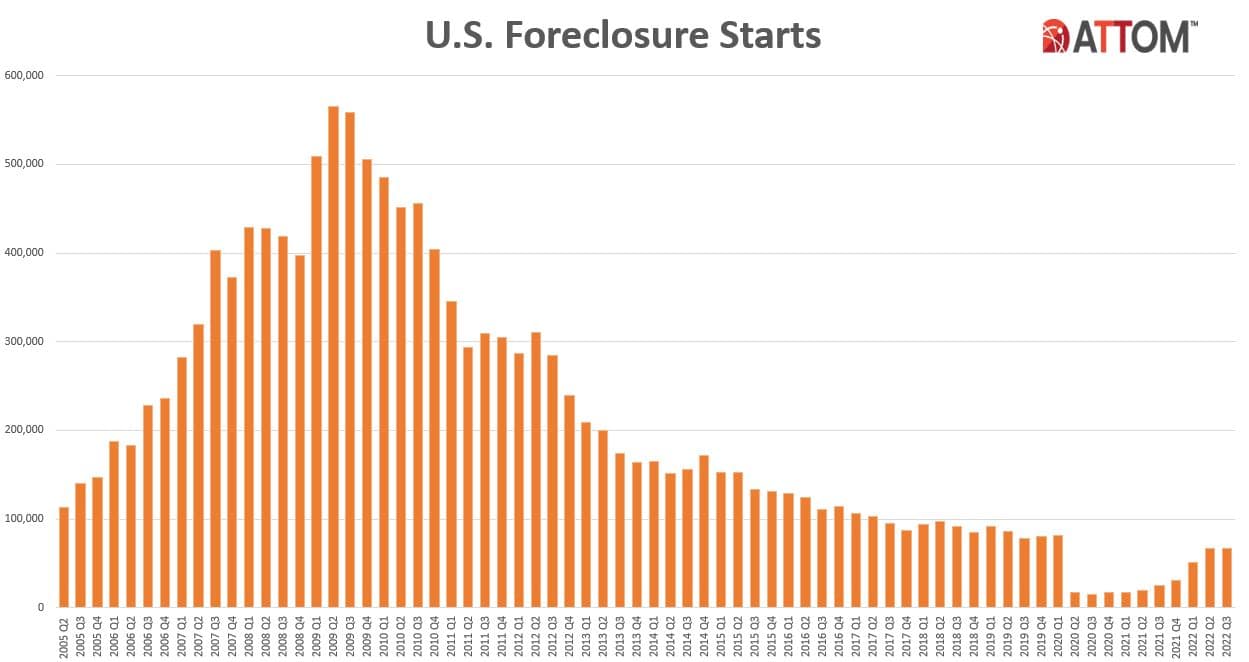

The Foreclosure Volume Is Nothing Like It Was During the Crash

Another difference is the number of homeowners that were facing foreclosure after the housing bubble burst. Foreclosure activity has been lower since the crash, largely because buyers today are more qualified and less likely to default on their loans. The graph below uses data from ATTOM Data Solutions to help paint the picture of how different things are this time:

Not to mention, homeowners today have options they just didn’t have in the housing crisis when so many people owed more on their mortgages than their homes were worth. Today, many homeowners are equity rich. That equity comes, in large part, from the way home prices have appreciated over time. According to CoreLogic:

“The total average equity per borrower has now reached almost $300,000, the highest in the data series.”

Rick Sharga, Executive VP of Market Intelligence at ATTOM Data, explains the impact this has:

“Very few of the properties entering the foreclosure process have reverted to the lender at the end of the foreclosure. . . . We believe that this may be an indication that borrowers are leveraging their equity and selling their homes rather than risking the loss of their equity in a foreclosure auction.”

This goes to show homeowners are in a completely different position this time. For those facing challenges today, many have the option to use their equity to sell their house and avoid the foreclosure process.

Bottom Line

If you’re concerned we’re making the same mistakes that led to the housing crash, the graphs above should help alleviate your fears. Concrete data and expert insights clearly show why this is nothing like the last time.

Since the 2008 housing bubble burst, the word recession strikes a stronger emotional chord than it ever did before. And while there’s some debate around whether we’re officially in a recession right now, the good news is experts say a recession today would likely be mild and the economy would rebound quickly. As the 2022 CEO Outlook from KPMG says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

To add to that sentiment, housing is typically one of the first sectors to rebound during a slowdown. As Ali Wolf, Chief Economist at Zonda, explains:

“Housing is traditionally one of the first sectors to slow as the economy shifts but is also one of the first to rebound.”

Part of that rebound is tied to what has historically happened to mortgage rates during recessions. Here’s a look back at rates during previous economic slowdowns to help put your mind at ease.

Mortgage Rates Typically Fall During Recessions

Historical data helps paint the picture of how a recession could impact the cost of financing a home. Looking at recessions in this country going all the way back to 1980, the graph below shows each time the economy slowed down mortgage rates decreased.

Fortuneexplains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

While history doesn’t always repeat itself, we can learn from and find comfort in the trends of what’s happened in the past. If you’re thinking about buying or selling a home, you can make the best decision by working with a trusted real estate professional. That way you have expert advice on what a recession could mean for the housing market.

Bottom Line

History shows you don’t need to fear the word recession when it comes to the housing market. If you have questions about what’s happening today, let’s connect so you have expert advice and insights you can trust.

![Applying for a Mortgage Doesn’t Have To Be Scary [INFOGRAPHIC] | Simplifying The Market](https://i2.wp.com/files.simplifyingthemarket.com/wp-content/uploads/2022/10/27090556/applying-for-a-mortgage-doesnt-have-to-be-scary-KCM-549x300.png?w=358&ssl=1)

![Applying for a Mortgage Doesn’t Have To Be Scary [INFOGRAPHIC] | Simplifying The Market](https://i1.wp.com/files.simplifyingthemarket.com/wp-content/uploads/2022/10/27090552/applying-for-a-mortgage-doesnt-have-to-be-scary-MEM.png?ssl=1)

{kind=link}